How Woodside uses a consultancy report to deflect responsibility for its emissions

Woodside Energy has cited a consultancy report it commissioned when countering scientific research linking its Scarborough project to climate-related deaths and coral bleaching. We asked for the full methodology. We got no reply. But even from what little has been made public, the integrity issues are clear.

Fossil fuel companies and their industry associations are engaging consultancies to produce ‘independent’ analysis – material they then use to justify climate-damaging projects and lobby governments for further approvals. But as we’ve previously shown, these reports can contain deeply flawed modelling and lack rigour, using optimistic assumptions and selective framing to generate outputs that suit industry but mislead the public and policy makers. Woodside Energy's use of a commissioned ACIL Allen report to defend its Scarborough Energy Project is a case in point.

This report has been frequently cited by the company, including on its own 'Fact Checker' webpage, in its submission to the Productivity Commission lobbying against a proposed tax on large corporations, and in media responses. Most recently, it was used by Woodside to respond to a media story about groundbreaking research which quantified the likely climate impacts – measured in millions of coral deaths and hundreds heat-related human deaths – of the company’s Scarborough gas project.

When the story ran on the ABC, Woodside gave a written response, which included citing the consultant’s report:

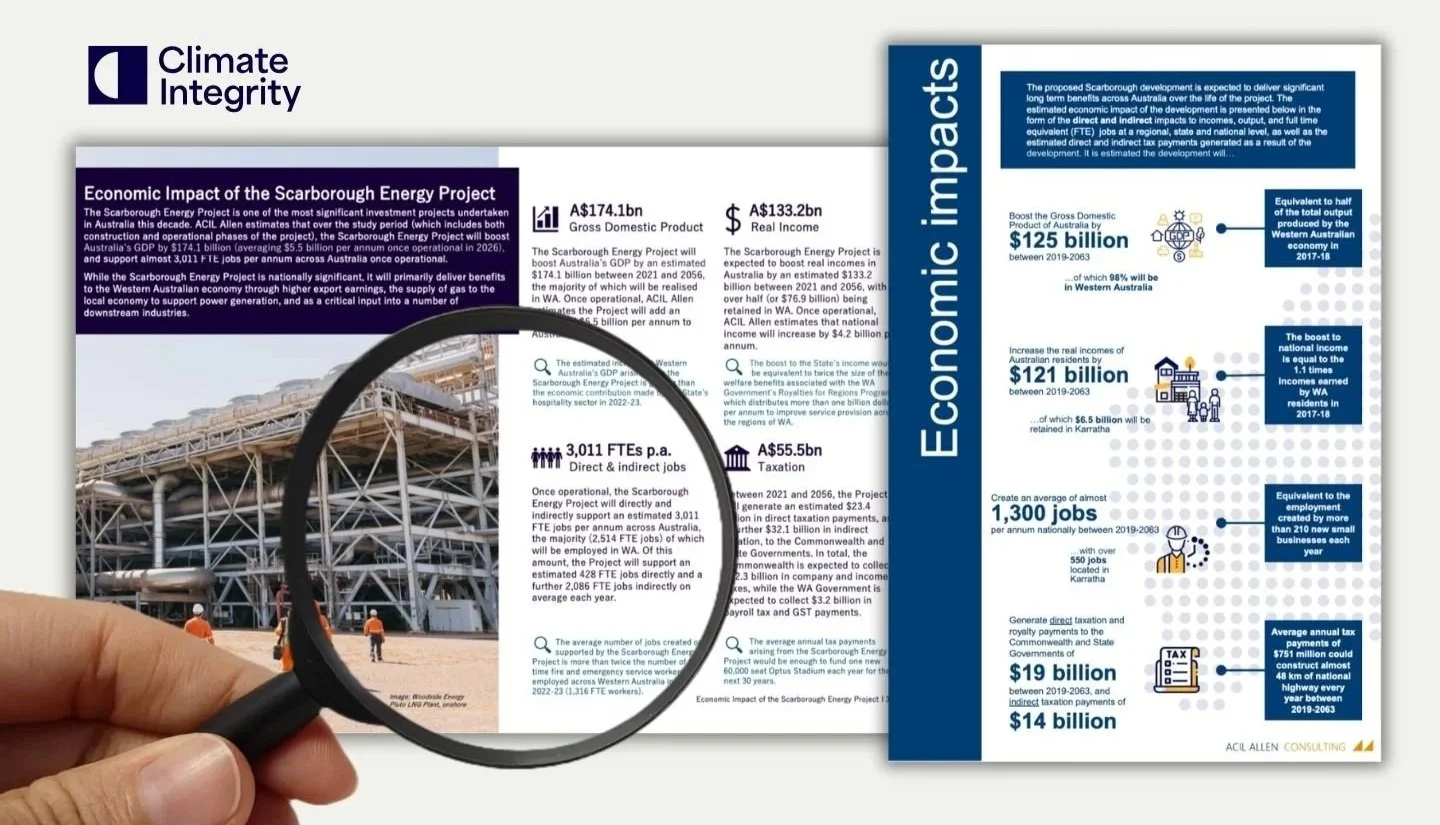

“A report prepared by consultancy ACIL Allen has found that Woodside’s Scarborough Energy Project is expected to generate an estimated A$52.8 billion in taxation and royalty payments, boost GDP by billions of dollars between 2024 and 2056 and employ 3,200 people during peak construction in Western Australia.”

Capture from Woodside’s website’s “Fact Checker”

What follows is an examination of the report’s claims. It is worth noting at the outset that Woodside and ACIL Allen have published two versions of this report – a 2019 original and a 2025 update – yet neither has ever been released in full. Only a four-page “summary report” has ever been made public, with all methodology and assumptions compressed into a textbox.

We contacted both Woodside and ACIL Allen requesting the full document. Neither responded. Ahead of publication we also provided both organisations with a formal right of reply, including specific questions (see below) about the report's methodology, assumptions, and version-to-version discrepancies. Neither responded to that either.

-

The 2019 and 2025 documents are described as "summary reports." Does a full underlying report exist for each, containing the complete model inputs, assumptions, scenario specifications and sensitivity analyses? If so, will Woodside make it publicly available?

The study period shortened by nine years between the 2019 and 2025 reports – from 2019–2063 to 2021–2056 – yet the headline GDP contribution rose from $125 billion to $174.1 billion. Can Woodside provide a like-for-like reconciliation of these figures, including the input assumptions that changed between versions?

Both reports list "carbon payments" as a component of direct taxation. What carbon price per tonne was assumed in each report, to what volume of emissions was it applied?

No scenario analysis, or sensitivity analysis, is presented in either report – can you provide the equivalent analysis under IEA APS and NZE price assumptions?

In the event that the Scarborough project is wound up before the end of its projected life – whether due to market conditions, policy change, or financial difficulty – who bears the decommissioning and site restoration costs? Has any contingent public liability been quantified, and if so, where is it disclosed?

-

The 2019 and 2025 documents are described as "summary reports." Does a full underlying report exist for each, containing the complete model inputs, assumptions, scenario specifications and sensitivity analyses? If so, will ACIL Allen make it publicly available?

Was the decision to use CGE modelling rather than a Cost-Benefit Analysis a decision made by ACIL Allen on methodological grounds, or a product of the scope specified by Woodside as the client?

Neither report discloses a discount rate. Do the GDP and income figures represent undiscounted real values? If so, what is the net present value of the project's economic contribution at a standard social discount rate, and why was this not reported?

Both reports list "carbon payments" as a component of direct taxation. What carbon price per tonne was assumed in each report, to what volume of emissions was it applied?

The national jobs figure more than doubled between reports – from approximately 1,300 FTE p.a. to 3,011 FTE p.a., with the direct operational headcount essentially unchanged at ~600. What changed in the indirect employment assumptions between 2019 and 2025, and can ACIL Allen provide the multiplier values used in each version?

Both reports state that all construction and operational spending data was supplied by Woodside. What independent verification of those inputs did ACIL Allen undertake, and does ACIL Allen stand behind the accuracy of the cost and revenue figures that drive the economic impact results?

What’s wrong with the report?

Without access to the full methodology it’s impossible for us – or anyone – to comprehensively assess the report’s claims. But across the two versions we can see a pattern that is problematic: benefits are padded with unrelated economic activity, costs are ignored, and figures change dramatically between versions with no explanation offered.

-

The report's headline employment figure – "3,011 FTE jobs per annum" – is not the full story. Just 600 of these are long-term, direct, full-time roles. From a $12.5 billion investment, that is roughly $20.8 million per job – reflecting poor job creation by any measure. The remaining positions are either temporary construction roles that peak at 3,200 during the build phase and then disappear, or indirect jobs derived from speculative economic multiplier effects.

Those multiplier-derived figures deserve particular scrutiny. Between the 2019 and 2025 versions of the report, the total jobs figure more than doubled – from 1,300 FTE jobs per annum nationally to 3,011 – despite using identical underlying price assumptions. Since the full methodology has never been disclosed, it is impossible to know whether this reflects genuine new economic analysis or simply a choice to apply more generous multipliers to produce a larger number. Without transparency over those assumptions, the headline figure cannot be taken at face value.

-

The 2025 report claims the project will generate $55.5 billion in "taxation" – but a closer look reveals more than half – $32.1 billion – is "indirect" taxation, which has no meaningful relationship to Woodside's own tax obligations. Including flow-on taxation from a kebab shop in Karratha in a headline figure attributed to the project is, at best, misleading. Indirect tax is also the easiest component to inflate – it flows through economic models whose outputs are highly sensitive to assumptions and opaque to outside scrutiny.

It’s also concerning that the figure for indirect taxation more than doubled between Woodside's 2019 and 2025 reports – from $14 billion to $32.1 billion. This is despite the study period shortening by 9 years and all disclosed assumptions remaining identical. This change demands an explanation that neither report provides.

The remaining $23.4 billion in "direct" taxation is itself a broader category than it is framed, incorporating:

"company tax"

"PRRT"

"payroll tax"

"development-specific royalties"

"condensate excise", and

"carbon payments".

Two of these are not taxes in any conventional sense of the word – royalties are payments for the right to extract a publicly-owned resource, and carbon payments are a regulatory compliance cost. Of the remainder, PRRT and company tax represent the bulk, but both are subject to rules that allow Woodside to defer meaningful payments for decades, as massive construction costs, debt deductions, and compounding PRRT credits shelter income well into the project's life. As Senator David Pocock recently pointed out, Australia collects $1.2 billion more from the beer tax than it does from the Petroleum Resource Rent Tax (PRRT). Payments are unlikely before the 2040s – by which point, at a standard 7% discount rate, the present value of those future flows would be roughly 75% lower than the headline figure suggests. The $55.5 billion offers no such adjustment.

-

The report claims the Scarborough project will boost Australia's GDP by $174.1 billion between 2021 and 2056. Once disaggregated, that averages $5.5 billion per year once operational – roughly 0.2% of Australia's current GDP, although even this needs to be taken with a grain of salt.

In the 2019 version of the report, the GDP figure was $125 billion – covering a 44-year period. By 2025 it had grown to $174.1 billion, despite the study period shrinking to 35 years. Even after adjusting for inflation, this is a 40% increase in annual GDP contribution between the 2019 and 2025 reports, with no disclosed change in methodology. The oil price assumption is identical. The input data still comes from Woodside. The only explanation on offer is a proprietary model that the public cannot scrutinise.

-

The report makes no mention of the carbon cost of 876 million tonnes of CO₂e – the very figure that the attribution research linked to 484 additional heat-related deaths in Europe alone and 16 million additional coral deaths on the Great Barrier Reef. It is also silent on decommissioning costs, stranded asset risk, and the opportunity cost of deploying US$12.5 billion into gas rather than renewables. A report that tallies benefits while failing to acknowledge any of these costs is not economic impact analysis – it is a brochure.

Who actually benefits?

The report claims the economic benefits of the entire Scarborough development – and almost anything that touches it – yet says little about where those benefits flow, or who bears the costs when they don't.

A significant portion of Woodside's institutional ownership sits offshore. US asset managers Vanguard and BlackRock alone hold over 12% of the company; the joint venture partner, INPEX, is Japanese. But even setting geography aside, share ownership is among the most unequally distributed forms of wealth. In the United States – whose asset managers hold some of the largest stakes in Woodside – the wealthiest 1% own 50% of all public equity. Similarly in Australia, the RBA reported that 10% of households hold 45% of all liquid assets, while the entire bottom half share just 2%.

The costs, meanwhile, fall on people entirely absent from this report. The Murujuga Aboriginal people whose rock art sits adjacent to the Burrup processing facility bear the local environmental burden. Fishing and tourism industries dependent on a functioning reef absorb the costs of coral bleaching. And households and governments globally will carry the climate harms that attribution science can now directly link to this project. None of this appears in ACIL Allen's ledger – because none of it is Woodside's cost to count.

What needs to change?

Commissioned reports convey independence and authority. That is precisely why the fossil fuel industry uses them – to shape public opinion, lobby government, and provide cover against inconvenient science.

Australia cannot make good decisions about its economic and climate future if the information underpinning those decisions is selectively framed, methodologically opaque, and inaccessible to public scrutiny. When companies like Woodside cite proprietary modelling to contest peer-reviewed research or influence policy, they should be required to publish the full methodology behind it.

The onus is also on consultancy firms. ACIL Allen is a legitimate and respected firm. But legitimate firms must take responsibility for the use to which their work is put. Producing analysis that systematically inflates benefits, ignores costs, and is then deployed to justify climate-damaging projects – while declining to make the full methodology public – is not consistent with professional integrity. Consultancies must be willing to insist that their methodology is publicly disclosed when their work is used in public debate or government submissions.

Woodside says it is transparent about all of its business activities. Releasing the full ACIL Allen report would be a good place to start.